What is Dalal Street Week Ahead: Traders exercise caution and hope the inflation number is good?

Dalal Street Week Ahead: Traders exercise caution and hope the inflation number is good is a trending topic covered by Sejal News Network with latest updates and insights.

The India VIX, which gauges anticipated market volatility, dropped dramatically during the week, particularly following the conclusion of big events (budget and FOMC meet last week). Therefore, if volatility continues to decline and hold at this level, there may be more market stability, which can reassure bulls further, according to experts.

In the week that concluded February 10, there was little trading on the market, and the benchmark indices mostly closed flat. In line with predictions, the Reserve Bank of India increased the repo rate by 25 basis points to 6.5 percent. The bank also changed its tone, raising its growth projection for FY23 to 7 percent, which improved the market’s attitude.

Gains were however constrained by the growing likelihood of further Federal Reserve policy tightening, particularly in light of recent economic data and FII outflow.

The Nifty Midcap 100 and Smallcap 100 indices posted nearly 2 percent and 1 percent gains, respectively, while the BSE Sensex dropped 159 points to 60,683 and the Nifty50 increased 2.5 points to 17,856. The broader markets outperformed the benchmarks.

Stocks in the automotive, energy, FMCG, metal, and oil and gas industries were under pressure, although purchases were made of certain banking and financial services, technology, and infrastructural companies.

The market’s initial response on Monday will be to monthly industrial output data that showed a slowdown to 4.3 percent (from 7.3 percent in November 2022). Overall, it is anticipated that the consolidation and rangebound trade we have been seeing for about one and a half months will continue in the upcoming week as well. As the quarter’s earnings season comes to a conclusion, the market will mostly be focused on monthly inflation data from India and the US, as well as stocks belonging to the Adani Group, according to experts.

Latest News

- The Story of Ameya Somvanshi: The 18-Year-Old Visionary Building an Empire Before Most Start Their Careers

- Rose & Rabbit Launches 100% Vegan Creamy Facial Wash: Cruelty-Free Cleansing Made in India for Indian Skin

- Sai Tamhankar Recalls Uncomfortable Bus Incident: “He Grabbed My Waist”

- Sonu Nigam Sings for Doctors During Hand Surgery, Viral Video Leaves Fans Amazed

- Pradeep Rawat’s Son Breaks Down at Prayer Meet, Promises to Carry Forward His Father’s Legacy

According to Vinod Nair, Head of Research at Geojit Financial Services, “moving forward, markets anticipate the release of important inflation statistics for a clear direction and to measure the strength of the economy.”

Investors need to use value buying as a strategy in these uncertain times. Smallcap companies appear alluring in the long run due to a decline in value towards the long-term averages, he suggested.

Let’s look at the 10 main elements that will probably keep traders busy the following week.

1) CPI Inflation :

The monthly CPI inflation data, which the street will be most interested in next week, has fallen for four consecutive months and has been below the upper bound of the RBI’s long-term target (4 percent and +/- 2 percent) for the past two months.

Even though core inflation is predicted to remain stable at or below 6 percent in the first month of 2023, the RBI’s Monetary Policy Committee hiked the repo rate by 25 basis points while maintaining its “removal of accommodation” stance.

“We anticipate that the CPI inflation rate in January stayed stable at 5.8 percent year over year, up slightly from 5.72 percent in December. While food prices are still declining and core inflation is still sticky, we anticipate the difference between the two to shrink in January as base effects affect food prices and core inflation consecutively ,” “At Barclays, Rahul Bajoria is the MD and Head of EM Asia (ex-China) Economics.

After eight consecutive months of readings between 6.2 and 6.3 percent, Bajoria anticipates core inflation to have dipped to 6 percent YoY in January.

“We anticipate modest slowing in core prices sequentially, along with a larger base since last month, as corporate profit margins moderate from historically high levels. But we still anticipate that rising pricing power and revived domestic demand would keep core inflation stable for longer “added he.

On February 14, the WPI inflation print will be revealed, followed by the January balance of trade statistics, the foreign currency reserves on the following day.

2) US Inflation :

Investors around the world will be paying close attention to the US inflation report, which is due out on February 14. This is because US inflation is a key factor in the Federal Reserve’s decision on interest rates for the upcoming month, and because the US dollar index has risen from 101.22 to 103.58 since the beginning of February amid concerns that inflation may tick up slightly in light of the positive jobs data. US bond yields increased over this time, from 3.42 percent to 3.74 percent.

For now, most experts anticipate it will decline even further in January 2023 from 6.5 percent in December.

Officials from the Fed made hints that they would continue to tighten policy until they saw clear evidence of future inflation decreasing.

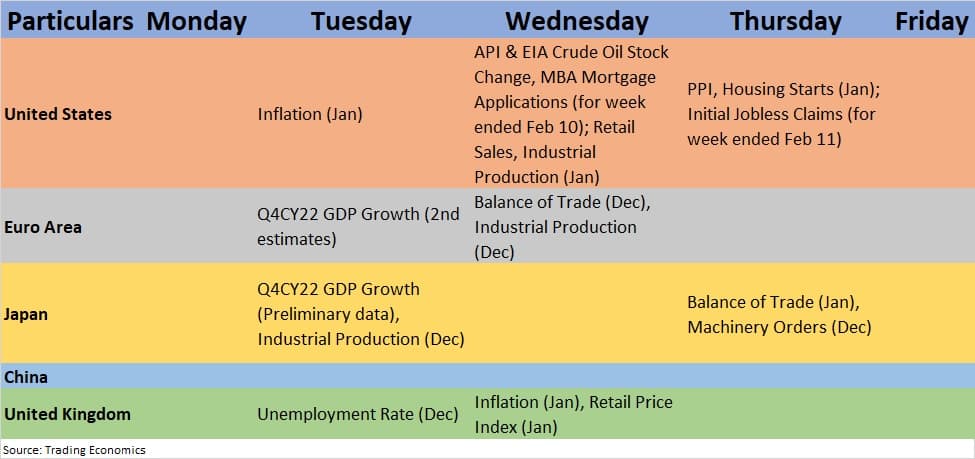

3) Global Economic Data Points

Here are key global economic data points to watch out for next week:

4) Corporate Earnings :

We are in the final stretch of the corporate earnings season, and over 1,500 companies will report their quarterly results the following week. The majority of results will be released within the first two days of the week.

Nykaa, Adani Enterprises, Eicher Motors, Grasim Industries, ONGC, Siemens, and Nestle India are significant companies to keep an eye on.

Additionally, Power Finance Corporation, Sun Pharma Advanced Research Company, Shree Renuka Sugars, SAIL, Wockhardt, Campus Activewear, Gujarat Gas, IRB Infrastructure Developers, Shalimar Paints, and Apollo Hospitals Enterprises. Next week will also see the announcement of the quarterly results from Bata India, Bharat Forge, Biocon, Bosch, Indiabulls Housing Finance, Ipca Laboratories, Prestige Estates Projects, and SpiceJet.

5) Oil Prices :

The street will also be paying attention to oil prices, which have seen a significant increase in the past week following Moscow’s decision to reduce oil production by 5 lakh barrels per day in March, particularly in light of Western countries’ bans on Russian oil and products in light of the ongoing Ukraine-Russian war. According to CNBC, the move was not discussed with the OPEC+ group, which Moscow co-chairs.

International benchmark Brent crude futures experienced a huge week-long increase, rising to $86.52 per barrel on Friday from just under $80 the previous week. However, the average price of a barrel has been below $90 for more than two and a half months, which analysts believe is not a major concern for India, the world’s largest net importer of oil.

6) FII Flow :

Last but not least, FII outflow was much reduced in February after a large outflow in January. If this trend continues, experts believe the market will be greatly supported, with the Nifty50 perhaps moving upward rather than downward.

“FIIs slowed down their selling in February and switched to buying for Rs 1,458 crore on February 10 after selling a significant amount of equities for Rs 53,887 crore in the cash market in January. The FPI’s strategy of shorting India and buying into more affordable countries like China, Hong Kong, and South Korea appears to be coming to an end “Chief Investment Strategist at Geojit Financial Services, V K Vijayakumar, said.

According to preliminary data from the NSE, FIIs have net sold more than Rs 5,000 crore worth of shares so far in February, but DIIs have made up for this by purchasing more than Rs 6,000 crore worth of shares over the same period.

7) Technical View :

On both the weekly and daily charts for the Nifty, a Doji-like pattern has formed, signifying uncertainty among buyers and sellers on the direction of the market. It traded consistently within the Budget day range for seven sessions in a row.

There are more chances than not for the rangebound trade to break upward rather than downward given the recent consolidation within the 17,650–17,900 range and the strong defence at 17,800. Additionally, if the Nifty50 manages to decisively break the downward-sloping resistance trend line adjacent to the highs of December 1, 2022, and January 24, 2023, which in large part also coincides with the high of Budget Day (17,972), there could be a rally towards 18,0. The tight budget day can be the first vital help (17,350).

“Nifty has been gradually moving upward, but it hasn’t yet displayed strong momentum. Prior to psychological level 18,000, we need it to break over Budget Day High of 17,970 “According to Waves Strategy Advisors’ founder and CEO, Ashish Kyal.

Any closure above 18,000 in his opinion will signal the beginning of a new uptrend. The wider market needs to participate, which is something that hasn’t happened yet, he added.

8) F&O Cues :

Additionally, according to option data, the Nifty50 is anticipated to face significant resistance at 18,000 in the short future, with support being in the range of 17,700–17,800.

Maximum Call open interest was at strike 18, followed by strikes 18,500 and 18,200, while Call writing was at strike 17,800, followed by strikes 18,000 and 18,200.

Maximum open interest was shown on the put side at strike 17,800, followed by strikes 17,000 and 17,500, and writing was seen at strike 17,800, followed by strikes 17,400 and 17,300.

As stated by Santosh Meena, Head of Research at Swastika Investmart, “Taking into account the derivative data, FIIs’ short exposure in index futures still remains at 82 percent and the put/call ratio is lying at the 1.02 level, there is opportunity for a short-covering recovery.”

9) India VIX :

The India VIX, which gauges anticipated market volatility, dropped dramatically during the week, particularly following the conclusion of big events (budget and FOMC meet last week). Therefore, if volatility continues to decline and hold at its current level, there may be more market stability, which can reassure bulls more, according to experts.

On a week-to-week basis, the volatility decreased by 11.46 percent, from a level of 14.40 to a level of 12.75.

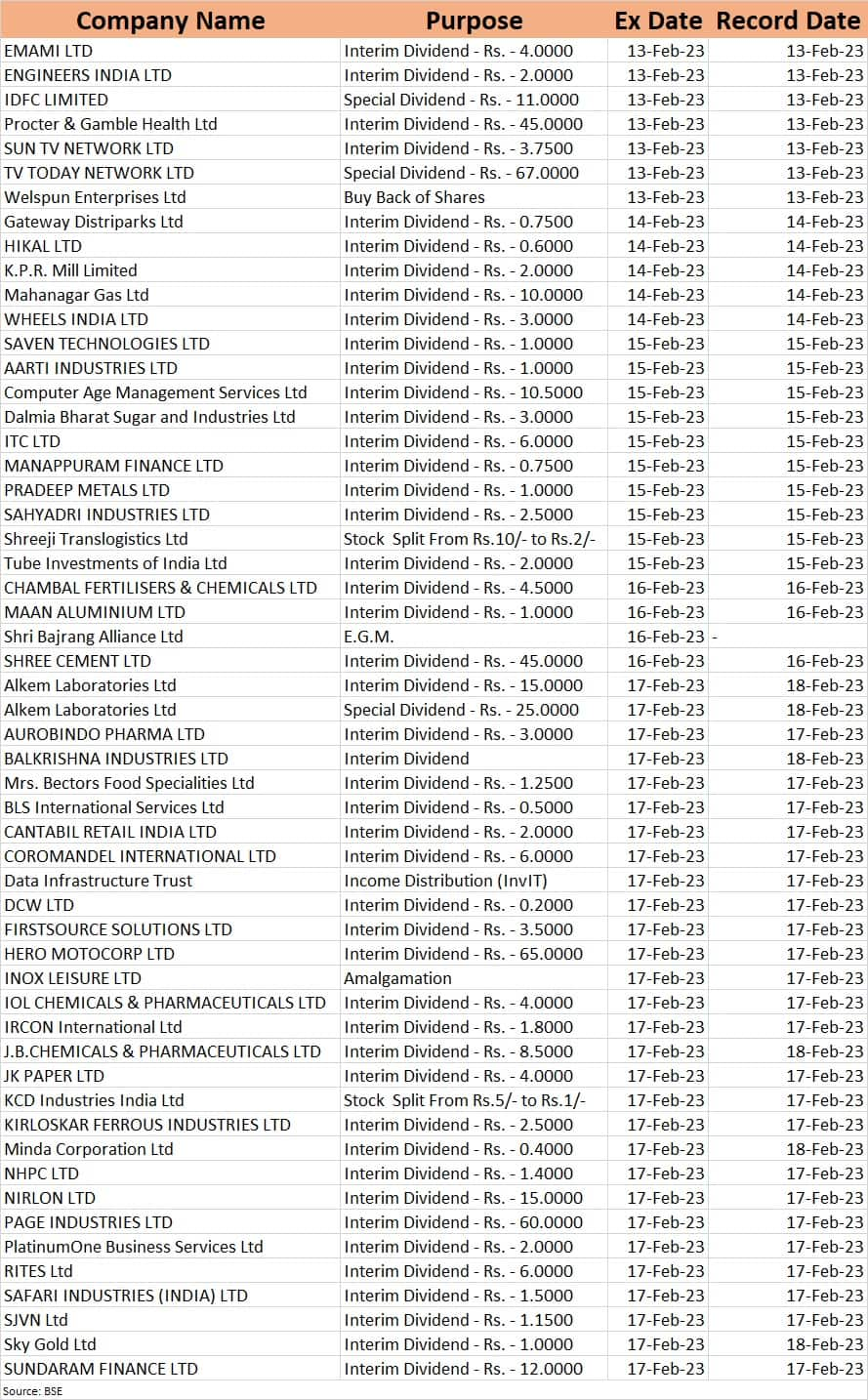

10) Corporate Action

The following are significant corporate events that will occur this week:

Related News

- UP Man Arrested for Breaching National Security in Collaboration with Pakistani Spy

- Shaswat Abhijeet Ghosh: A Visionary Leader in Business and Philanthropy

- Investing in Freedom: The Advantages of Buying a Residential Plot